為何中國能比美國更快地擺脫疫情陰霾,走上復蘇之路?

錢科雷(Clay Chandler)

2020-04-24

許多經濟學家則預測,美國經濟將在今年剩余時間里放緩,甚至負增長,而中國經濟則有望在下半年反彈。

文本設置

文本設置

Plus(0條)

Plus(0條)

正如上周相繼公布的兩項嚴峻的統計數據所示,新冠病毒已經讓世界上最大的兩個經濟體停擺。

4月16日,美國勞工部報告稱,過去四周,失業救濟申請人數超過2,200萬,比美國經濟在過去九年創造的所有就業崗位還要多。4月17日,中國國家統計局宣布,中國1月至3月之間GDP下降了6.8%,創下數十年來的季度跌幅紀錄。

然而,就像一些病毒感染者比其他患者康復得更快一樣,中美兩國經濟很可能以不同的速度復蘇。這場危機爆發前,美國經濟穩步增長,消費者信心高漲,失業率接近歷史低點,可謂風頭正勁。中國經濟則呈現趨緩跡象。特朗普總統信誓旦旦地承諾稱,一旦新冠疫情得到遏制,美國經濟將“像火箭起飛一樣”迅速增長。

但是,許多經濟學家則預測,美國經濟將在今年剩余時間里放緩,甚至負增長,而中國經濟則有望在下半年反彈。

“我覺得,美國的處境顯然更艱難,因為它應對疫情的時間點晚于中國,封鎖措施也不像中國那樣全面。”北京佳富龍洲咨詢公司的經濟學家葛藝豪說。

供職于私營部門的經濟學家中,越來越多的人認為中國經濟將在本季度出現轉機,這并不是說他們認為中國經濟會迎來V型反轉,即經濟增長會像它突然消失一樣迅速反彈。但的確,一些經濟學家預計,中國經濟將在今年的最后三個月逐漸恢復到危機前接近6%的增長率。

中國3月的數據顯示,與1月和2月相比,零售額、用電量和固定資產投資的下滑速度有所放緩,汽車銷量則大幅上揚。馬修亞洲基金管理公司的投資策略師羅福萬據此認為,這表明中國已經“走上復蘇之路”。

中國經濟峰回路轉的另一個跡象是:法國奢侈品巨頭路威酩軒集團表示,中國內地路易·威登門店在過去三周的銷售額跟去年同期相比增長了50%。歐萊雅的首席執行官安鞏在4月16日透露稱,該公司3月的在華銷售額轉為正,本月可能會增長5%至10%。

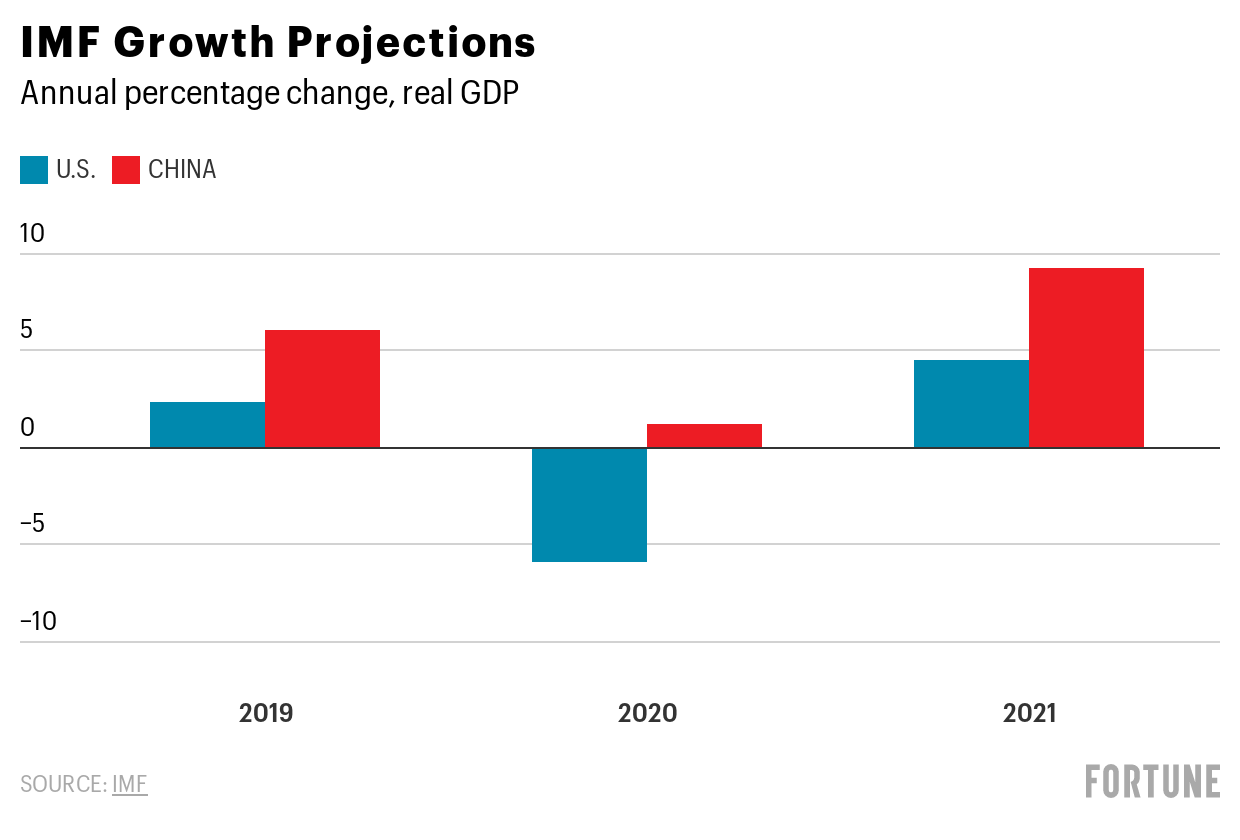

4月15日,國際貨幣基金組織發布報告,預計2020年中國國內生產總值較上一年增長1.2%,還將在2021年飆漲9.2%。該組織預計,2020年美國經濟將萎縮5.9%,然后在2021年增長4.7%。羅福萬認為,IMF對兩大經濟體增長前景的預測“都過高了,但總體來說,我是認同這種趨勢的。”

這場大疫情已經導致兩國都有數百萬人失業,但美國的失業人數看起來要高得多。中國的城鎮調查失業率多年保持在5%左右,根據中國國家統計局最近發布的數據,這個數字在2月升至6.2%,已經算是創紀錄了。(值得注意的是,這些數據并沒有反映數百萬農民工的困境:春節期間,由于全國各地采取隔離措施,再加上工廠停工,大批返鄉過年的農民工無法重返工作崗位。)高盛集團預計,美國今年的失業率將超過15%,而2019年年底的失業率僅為3.5%。國會預算辦公室則認為,美國失業率在2021年年底之前,都將保持在9%上下。

中國比美國更容易重啟經濟的一個原因是,制造業工人在中國勞動人口中的占比遠高于美國。制造業約占中國GDP的40%,而美國的這一比例僅為11%左右。“推動工廠復工復產,遠比讓消費者重拾外出消費的習慣容易得多。”葛藝豪說。

對于中美兩國領導人來說,經濟何時復蘇,如何復蘇,都可能帶來挑戰。中國政府為2020年確定的官方增長目標為6%。但新冠疫情使得實現這一目標有一定難度。

而特朗普面臨的風險是,在11月大選投票日到來之際,美國將陷入衰退泥沼,與率先爆發疫情、經濟形勢卻明顯好轉的中國形成鮮明對比。

雖然中國的病毒傳播比美國早得多,但其對武漢及周邊地區6,000萬人口實施的嚴格隔離措施,成功使新增感染病例曲線趨于平緩。在武漢嚴格執行的封鎖舉措,從1月23日持續到了4月8日,但中國大部分地區的出行限制,早在2月中旬就已經放松。羅福萬在一份寫給客戶的報告中指出:“從3月的下半月開始,中國大部分地區的生活逐漸恢復常態。”

到4月中旬,中國每日新增感染病例的15天平均值已經從2月中旬疫情高峰期的近4,000例降至50例左右。在美國,截至4月15日的15天平均值出現放緩跡象,但仍然超過3萬例。到了4月19日,中國累計報告確診病例約8.4萬例,累計死亡病例4,700例,美國的累計確診病例約73.5萬例,死亡3.9萬人。

08年全球金融危機爆發后,中國政府為提振經濟而采取了4萬億人民幣的大規模刺激措施,但到目前為止,中國似乎無意重復這樣的舉措。根據彭博經濟研究的數據,中國為應對新冠疫情而宣布的財政刺激規模僅占其GDP的3%左右,而美國和日本的這一比例分別高達10%和20%。中國因此前的大量支出存在債務風險,整體債務規模已超過GDP的300%。

但羅福萬認為,即使沒有這種大規模刺激計劃,中國依然是“世界上最好的消費市場”,他說,對于跨國公司和全球投資者來說,中國很可能仍然是一個極富吸引力的投資目的地。(財富中文網)

譯者:任文科

正如上周相繼公布的兩項嚴峻的統計數據所示,新冠病毒已經讓世界上最大的兩個經濟體停擺。

4月16日,美國勞工部報告稱,過去四周,失業救濟申請人數超過2,200萬,比美國經濟在過去九年創造的所有就業崗位還要多。4月17日,中國國家統計局宣布,中國1月至3月之間GDP下降了6.8%,創下數十年來的季度跌幅紀錄。

然而,就像一些病毒感染者比其他患者康復得更快一樣,中美兩國經濟很可能以不同的速度復蘇。這場危機爆發前,美國經濟穩步增長,消費者信心高漲,失業率接近歷史低點,可謂風頭正勁。中國經濟則呈現趨緩跡象。特朗普總統信誓旦旦地承諾稱,一旦新冠疫情得到遏制,美國經濟將“像火箭起飛一樣”迅速增長。

但是,許多經濟學家則預測,美國經濟將在今年剩余時間里放緩,甚至負增長,而中國經濟則有望在下半年反彈。

“我覺得,美國的處境顯然更艱難,因為它應對疫情的時間點晚于中國,封鎖措施也不像中國那樣全面。”北京佳富龍洲咨詢公司的經濟學家葛藝豪說。

供職于私營部門的經濟學家中,越來越多的人認為中國經濟將在本季度出現轉機,這并不是說他們認為中國經濟會迎來V型反轉,即經濟增長會像它突然消失一樣迅速反彈。但的確,一些經濟學家預計,中國經濟將在今年的最后三個月逐漸恢復到危機前接近6%的增長率。

中國3月的數據顯示,與1月和2月相比,零售額、用電量和固定資產投資的下滑速度有所放緩,汽車銷量則大幅上揚。馬修亞洲基金管理公司的投資策略師羅福萬據此認為,這表明中國已經“走上復蘇之路”。

中國經濟峰回路轉的另一個跡象是:法國奢侈品巨頭路威酩軒集團表示,中國內地路易·威登門店在過去三周的銷售額跟去年同期相比增長了50%。歐萊雅的首席執行官安鞏在4月16日透露稱,該公司3月的在華銷售額轉為正,本月可能會增長5%至10%。

4月15日,國際貨幣基金組織發布報告,預計2020年中國國內生產總值較上一年增長1.2%,還將在2021年飆漲9.2%。該組織預計,2020年美國經濟將萎縮5.9%,然后在2021年增長4.7%。羅福萬認為,IMF對兩大經濟體增長前景的預測“都過高了,但總體來說,我是認同這種趨勢的。”

這場大疫情已經導致兩國都有數百萬人失業,但美國的失業人數看起來要高得多。中國的城鎮調查失業率多年保持在5%左右,根據中國國家統計局最近發布的數據,這個數字在2月升至6.2%,已經算是創紀錄了。(值得注意的是,這些數據并沒有反映數百萬農民工的困境:春節期間,由于全國各地采取隔離措施,再加上工廠停工,大批返鄉過年的農民工無法重返工作崗位。)高盛集團預計,美國今年的失業率將超過15%,而2019年年底的失業率僅為3.5%。國會預算辦公室則認為,美國失業率在2021年年底之前,都將保持在9%上下。

中國比美國更容易重啟經濟的一個原因是,制造業工人在中國勞動人口中的占比遠高于美國。制造業約占中國GDP的40%,而美國的這一比例僅為11%左右。“推動工廠復工復產,遠比讓消費者重拾外出消費的習慣容易得多。”葛藝豪說。

對于中美兩國領導人來說,經濟何時復蘇,如何復蘇,都可能帶來挑戰。中國政府為2020年確定的官方增長目標為6%。但新冠疫情使得實現這一目標有一定難度。

而特朗普面臨的風險是,在11月大選投票日到來之際,美國將陷入衰退泥沼,與率先爆發疫情、經濟形勢卻明顯好轉的中國形成鮮明對比。

雖然中國的病毒傳播比美國早得多,但其對武漢及周邊地區6,000萬人口實施的嚴格隔離措施,成功使新增感染病例曲線趨于平緩。在武漢嚴格執行的封鎖舉措,從1月23日持續到了4月8日,但中國大部分地區的出行限制,早在2月中旬就已經放松。羅福萬在一份寫給客戶的報告中指出:“從3月的下半月開始,中國大部分地區的生活逐漸恢復常態。”

到4月中旬,中國每日新增感染病例的15天平均值已經從2月中旬疫情高峰期的近4,000例降至50例左右。在美國,截至4月15日的15天平均值出現放緩跡象,但仍然超過3萬例。到了4月19日,中國累計報告確診病例約8.4萬例,累計死亡病例4,700例,美國的累計確診病例約73.5萬例,死亡3.9萬人。

08年全球金融危機爆發后,中國政府為提振經濟而采取了4萬億人民幣的大規模刺激措施,但到目前為止,中國似乎無意重復這樣的舉措。根據彭博經濟研究的數據,中國為應對新冠疫情而宣布的財政刺激規模僅占其GDP的3%左右,而美國和日本的這一比例分別高達10%和20%。中國因此前的大量支出存在債務風險,整體債務規模已超過GDP的300%。

但羅福萬認為,即使沒有這種大規模刺激計劃,中國依然是“世界上最好的消費市場”,他說,對于跨國公司和全球投資者來說,中國很可能仍然是一個極富吸引力的投資目的地。(財富中文網)

譯者:任文科

The coronavirus has brought the world’s two largest economies to their knees, as two grim statistics released this past week attest.

On April 16, the U.S. Labor Department reported that the number of Americans filing for unemployment benefits in the last four weeks topped 22 million—more jobs than the U.S. economy has created in the last nine years. On April 17, China's National Bureau of Statistics announced that between January and March, that nation's economy shrank 6.8%, the sharpest quarterly contraction since the tumult of Mao’s Cultural Revolution.

And yet, just as some patients infected with the virus get back on their feet more rapidly than others, the U.S. and Chinese economies likely will recover at different rates. Going into the crisis, the U.S. economy was strong—growth was steady, consumer confidence was high, unemployment neared all-time lows—while China's economy was slowing. President Donald Trump has promised that the U.S. economy will take off “like a rocketship” once the virus is contained.

Many economists, however, expect slow to negative growth in the U.S. through the rest of this year, even as China bounces back in the second half.

“I think clearly the U.S. has a tougher time because it reacted later [to the outbreak] than China and had a less comprehensive lockdown,” says Arthur Kroeber, an economist at GaveKal Dragonomics.

Among private economists, there is a growing consensus that China’s economy will turn the corner in the current quarter. Few are predicting a V-shaped recovery in which growth snaps back as suddenly as it disappeared. But some think the country could gradually return to a pre-crisis growth rate of close to 6% in the last three months of the year.

Andy Rothman, an investment strategist at Matthews Asia argues March data from China—which show slower declines in retail sales, electricity consumption, and fixed asset investment and a sharp uptick in auto sales compared to January and February—signal China already is “on the road to recovery.”

Another sign of China's brighter outlook: French luxury giant LVMH says sales in Louis Vuitton's mainland stores jumped 50% the last three weeks compared to the same period a year ago. L’Oreal chief executive officer Jean-Paul Agon said on April 16 that sales in China turned positive in March and will likely gain 5% to 10% this month.

On April 15, the International Monetary Fund forecasted China’s GDP for 2020 would rise by 1.2% over last year, then gain 9.2% in 2021. The Fund predicted the U.S. economy will contract by 5.9% in 2020 before rising 4.7% in 2021. Rothman says he considers the IMF’s projections for both economies “too high, but I agree with the overall trend.”

The crisis has wiped out millions of jobs in both countries, but the employment toll appears to be much greater in the U.S. China said its urban jobless rate, which has remained about 5% for years, rose to a record 6.2% in February. (It should be noted that those figures don't capture the plight of the millions of migrant laborers unable to return to work after China's Lunar New Year because of nationwide quarantines and factory closures.) Goldman Sachs expects the U.S. jobless rate to exceed 15% this year, up from just 3.5% at the end of 2019. The Congressional Budget Office projects unemployment to remain at 9% through 2021.

One reason it's easier for China to jumpstart growth versus the U.S. is that a higher percentage of Chinese workers are employed in the manufacturing sector, which accounts for about 40% of China's GDP compared to about 11% in the U.S. "It's much easier to restart factories than to get consumers back in the habit of going out and spending," says Kroeber.

For leaders in both nations, the timing and trajectory of recovery pose political challenges. China’s government had set an official growth target of 6% for 2020.

For Trump, the risk is that, come voting day in November, America will be mired in a recession even as China, where the virus originated, is visibly on the mend.

However belated, China’s draconian quarantine of 60 million people in Wuhan and surrounding Hubei province appears to have succeeded in flattening the curve of new infections at a much earlier stage than in the U.S. In Wuhan, a strictly enforced lockdown lasted from January 23 to April 8. But in much of the rest of the country, restrictions were eased as early as mid-February. Rothman, in a note to clients, observes that “across most of China, life began slowly returning to normal in the second half of March.”

By mid-April, the 15-day average of new infections per day in China had dropped to around 50, down from nearly 4,000 at the peak of the outbreak in mid-February. In the U.S., the 15-day average for the period ending April 15 showed signs of slowing, but exceeded 30,000. By early April 19, China had reported roughly 84,000 total infections with 4,700 deaths, while the U.S. had some 735,000 cases with 39,000 deaths.

So far China’s government has shown no inclination to repeat the kind of massive stimulus measures predecessors used to bolster growth after the Global Financial Crisis. Policies China has announced in response to the pandemic account for only about 3% of GDP, according to Bloomberg Economics, compared to 10% and 20% for Washington and Tokyo, respectively. That earlier spending spree pushed China’s debt-to-GDP ratio to more than 300%.

But even without such budget-busting, China remains the “world’s best consumer story,” according to Rothman, and likely to remain an attractive designation for multinationals and global investors.

請打開財富Plus APP