風投的好日子結束了,未來幾年都會很難

ADAM FELESKY

2022-07-23

繁榮時期的低息貸款已經一去不復返了。

文本設置

文本設置

Plus(0條)

Plus(0條)

這可能是電影大片季,但在金融科技投資領域,大型交易季已經過去了。在又一個創紀錄的融資年之后——2021年,全球風險投資融資規模達到6210億美元,比之前的高點輕松翻了一番——繁榮時期的低息貸款已經一去不復返了。

也就是說,最好的公司仍然可以獲得明智而有紀律的風險投資。

事必躬親而相沿成習的投資方法實施起來并不容易。這一方法的實施需要深入了解市場和大量資源,也需要紀律嚴明而嚴格縝密的決策過程。我們相信這種方法適用于所有周期,而且在充滿挑戰的市場中,其影響可能會變得更加明顯。

巨額融資周期和虛榮

在科技投資領域,我們迎來了輝煌的一年。多個行業的初創公司利用創紀錄的投資金額以對創始人友好的估值籌集了大量資金。在過去12個月里,僅Portage投資組合公司就從投資者那里籌集了近12億美元的資金。

伴隨著巨額融資,2021年獨角獸公司的總數也大幅增加。去年獨角獸公司總數達到959家,同比增長69%。

專注于虛榮標記,如獨角獸公司狀態,是我們接近“頂峰”的明確信號。在互聯網泡沫破裂的前夕,“訪問人數”(即每日/每月的獨立網站訪問者)是一個被大肆吹捧的指標。同樣,在打造一家實力雄厚的長期企業過程中,這種估值狀態是一種耗費精力的追求,而不是其他幾個重要數據點中的一個。

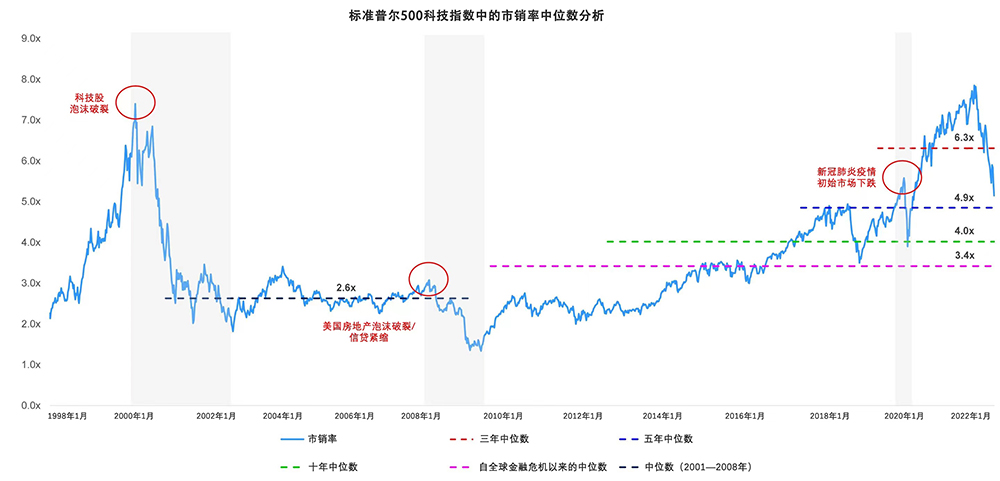

果然,如今繁榮周期已經結束。預期中的利率飆升、高通脹、當前的疫情和地緣政治緊張局勢正在導致市場出現動蕩。根據我們的計算,公共科技收入倍數在2021年12月達到峰值,為市銷率的7.85倍,截至2022年6月,為5.15倍,比迄今為止的峰值水平下降了34%。在通脹見頂之前,市場可能不會觸底。隨后可能會出現一段混亂時期,直到市場能夠順利通過下一個增長周期。

市場會變得多混亂,混亂會持續多長時間呢?如果過去只是一個序幕,我們或許可以從科技股在互聯網泡沫破裂和全球金融危機(GFC)期間的表現中學到一些經驗教訓。公共科技收入倍數在互聯網泡沫破裂期間壓縮了75%,在全球金融危機期間壓縮了60%。直到2014年11月,科技股才恢復到全球金融危機前的峰值水平。直到2021年8月,科技股才恢復到互聯網泡沫破裂前的峰值水平。

雖然我們無法預測未來,但隨著科技股市盈率迅速接近其五年中位數,我們有理由相信,這種情況需要數年時間才能逆轉。

作為戰時投資者

除非你的整個團隊都明白他們身處戰場,否則你不可能成為戰時投資者。首先,確保你的團隊了解市場環境已經發生了變化。

要將重點轉向你現有的投資組合,以了解誰面臨的風險最大以及需要采取哪些措施來降低失敗的風險。與其他投資者和管理層合作,然后開始行動——不要再等一兩個季度——不管你的財務狀況如何。戰時不會獎勵那些采取觀望態度的人。

在投資未來人力和資本資源的領域進行內部調整。遺憾的是,這兩者都是有限的,當資本來源枯竭時,風險投資的冪律就成了一個至關重要的考慮事項。在這種環境下,做出正確的大賭注是加倍重要的,因為已經在你投資組合中的公司更有可能希望你領導或支持他們未來幾輪融資。

將你的注意力轉移到有針對性的起源上。現在是時候通過深入研究、市場測繪和客戶盡職調查來優化和重新整合你的投資理念了。這也是樹立和嚴格測試投資理念的最佳時機。

要與盡可能多的公司會面。這可以歸結為了解為什么你是一家公司的差異化投資者,以及你可以采取哪些措施來推動其實現成功。

作為戰時首席執行官

如果你領導的是一家后期風險投資企業,第一步是相同的:確保你的團隊了解市場環境已經發生了重大變化。

但愿,你利用之前強勁的市場建立了專用基金,這樣在需要新資金之前至少有24個月的資金儲備。如果你有幸可以通過犧牲收入增長來實現盈虧平衡,那就這樣做吧。如果你無法通過犧牲收入增長來實現盈虧平衡,那就弄清楚這家公司在跑道盡頭需要變成什么樣才能吸引未來的投資者,哪些投資者可能比你在前幾輪融資中看到的投資者更有紀律。

這很可能意味著能夠展示有效增長、擴大毛利率和營業利潤率以及增強對未來盈利能力的預見。在行動中,這可以轉化為以激進的方式進行內部優先化。你必須堅決停止那些不能立即實現這三個原則的活動。

如果你是一家處于早期階段的企業,你必須與你的投資者在成功的定義上達成一致。這一點尤其重要,因為在很多情況下,你的下一個投資者可能就是你當前的投資者。如果你能夠從外部籌集資金,你很可能在充分了解自己定價權的基礎上,已經證明了某種形式的產品市場適合特定的細分市場。你這樣做的預算可能相當有限。一開始,你可能擁有一支出色的、充滿激情的、有使命感的團隊,現在他們開始吸引頂尖人才。最后,我敢打賭,你能簡明扼要地闡明你的使命有多重要、多遠大,以及為什么你會成為贏家。

世界新秩序

有些人可能會發現,投資最可愛的CryptoKittie游戲賺快錢比填寫電子表格或進行拆分測試更有趣,但增長周期的那個時段已經過去了。

但風險投資對投資者或創始人來說并不容易,而且理應如此。我們必須理解和適應新周期的變化。當下一個增長周期到來時,隨著倍數開始再次擴大,我們對最具潛力的初創公司的承諾和支持將獲得指數級的回報。(財富中文網)

亞當·費萊斯基(Adam Felesky)是Portage的聯合創始人兼首席執行官。

本評論文章僅代表作者個人觀點,并不代表《財富》雜志的觀點和立場。

譯者:中慧言-王芳

這可能是電影大片季,但在金融科技投資領域,大型交易季已經過去了。在又一個創紀錄的融資年之后——2021年,全球風險投資融資規模達到6210億美元,比之前的高點輕松翻了一番——繁榮時期的低息貸款已經一去不復返了。

也就是說,最好的公司仍然可以獲得明智而有紀律的風險投資。

事必躬親而相沿成習的投資方法實施起來并不容易。這一方法的實施需要深入了解市場和大量資源,也需要紀律嚴明而嚴格縝密的決策過程。我們相信這種方法適用于所有周期,而且在充滿挑戰的市場中,其影響可能會變得更加明顯。

巨額融資周期和虛榮

在科技投資領域,我們迎來了輝煌的一年。多個行業的初創公司利用創紀錄的投資金額以對創始人友好的估值籌集了大量資金。在過去12個月里,僅Portage投資組合公司就從投資者那里籌集了近12億美元的資金。

伴隨著巨額融資,2021年獨角獸公司的總數也大幅增加。去年獨角獸公司總數達到959家,同比增長69%。

專注于虛榮標記,如獨角獸公司狀態,是我們接近“頂峰”的明確信號。在互聯網泡沫破裂的前夕,“訪問人數”(即每日/每月的獨立網站訪問者)是一個被大肆吹捧的指標。同樣,在打造一家實力雄厚的長期企業過程中,這種估值狀態是一種耗費精力的追求,而不是其他幾個重要數據點中的一個。

果然,如今繁榮周期已經結束。預期中的利率飆升、高通脹、當前的疫情和地緣政治緊張局勢正在導致市場出現動蕩。根據我們的計算,公共科技收入倍數在2021年12月達到峰值,為市銷率的7.85倍,截至2022年6月,為5.15倍,比迄今為止的峰值水平下降了34%。在通脹見頂之前,市場可能不會觸底。隨后可能會出現一段混亂時期,直到市場能夠順利通過下一個增長周期。

市場會變得多混亂,混亂會持續多長時間呢?如果過去只是一個序幕,我們或許可以從科技股在互聯網泡沫破裂和全球金融危機(GFC)期間的表現中學到一些經驗教訓。公共科技收入倍數在互聯網泡沫破裂期間壓縮了75%,在全球金融危機期間壓縮了60%。直到2014年11月,科技股才恢復到全球金融危機前的峰值水平。直到2021年8月,科技股才恢復到互聯網泡沫破裂前的峰值水平。

雖然我們無法預測未來,但隨著科技股市盈率迅速接近其五年中位數,我們有理由相信,這種情況需要數年時間才能逆轉。

作為戰時投資者

除非你的整個團隊都明白他們身處戰場,否則你不可能成為戰時投資者。首先,確保你的團隊了解市場環境已經發生了變化。

要將重點轉向你現有的投資組合,以了解誰面臨的風險最大以及需要采取哪些措施來降低失敗的風險。與其他投資者和管理層合作,然后開始行動——不要再等一兩個季度——不管你的財務狀況如何。戰時不會獎勵那些采取觀望態度的人。

在投資未來人力和資本資源的領域進行內部調整。遺憾的是,這兩者都是有限的,當資本來源枯竭時,風險投資的冪律就成了一個至關重要的考慮事項。在這種環境下,做出正確的大賭注是加倍重要的,因為已經在你投資組合中的公司更有可能希望你領導或支持他們未來幾輪融資。

將你的注意力轉移到有針對性的起源上。現在是時候通過深入研究、市場測繪和客戶盡職調查來優化和重新整合你的投資理念了。這也是樹立和嚴格測試投資理念的最佳時機。

要與盡可能多的公司會面。這可以歸結為了解為什么你是一家公司的差異化投資者,以及你可以采取哪些措施來推動其實現成功。

作為戰時首席執行官

如果你領導的是一家后期風險投資企業,第一步是相同的:確保你的團隊了解市場環境已經發生了重大變化。

但愿,你利用之前強勁的市場建立了專用基金,這樣在需要新資金之前至少有24個月的資金儲備。如果你有幸可以通過犧牲收入增長來實現盈虧平衡,那就這樣做吧。如果你無法通過犧牲收入增長來實現盈虧平衡,那就弄清楚這家公司在跑道盡頭需要變成什么樣才能吸引未來的投資者,哪些投資者可能比你在前幾輪融資中看到的投資者更有紀律。

這很可能意味著能夠展示有效增長、擴大毛利率和營業利潤率以及增強對未來盈利能力的預見。在行動中,這可以轉化為以激進的方式進行內部優先化。你必須堅決停止那些不能立即實現這三個原則的活動。

如果你是一家處于早期階段的企業,你必須與你的投資者在成功的定義上達成一致。這一點尤其重要,因為在很多情況下,你的下一個投資者可能就是你當前的投資者。如果你能夠從外部籌集資金,你很可能在充分了解自己定價權的基礎上,已經證明了某種形式的產品市場適合特定的細分市場。你這樣做的預算可能相當有限。一開始,你可能擁有一支出色的、充滿激情的、有使命感的團隊,現在他們開始吸引頂尖人才。最后,我敢打賭,你能簡明扼要地闡明你的使命有多重要、多遠大,以及為什么你會成為贏家。

世界新秩序

有些人可能會發現,投資最可愛的CryptoKittie游戲賺快錢比填寫電子表格或進行拆分測試更有趣,但增長周期的那個時段已經過去了。

但風險投資對投資者或創始人來說并不容易,而且理應如此。我們必須理解和適應新周期的變化。當下一個增長周期到來時,隨著倍數開始再次擴大,我們對最具潛力的初創公司的承諾和支持將獲得指數級的回報。(財富中文網)

亞當·費萊斯基(Adam Felesky)是Portage的聯合創始人兼首席執行官。

本評論文章僅代表作者個人觀點,并不代表《財富》雜志的觀點和立場。

譯者:中慧言-王芳

It may be blockbuster season at the movies, but over in the fintech investment space, the season for mega deals has passed. After yet another year of record-breaking funding—2021 saw $621?billion in global venture capital financing, easily doubling the previous high—the easy money of boom days is gone.

That said, smart, disciplined venture capital investment is still available for the best companies.

A hands-on, prescriptive investment approach is not easy. It requires in-depth knowledge of the market and significant resources combined with a disciplined and rigorous decision-making process. We believe in this approach in all cycles, and that its impact may become even clearer in a challenging market.

The blockbuster cycle and vanity

We are coming off a banner year in the tech investment space. Startups across several industries took advantage of record-breaking investment numbers to raise tons of capital at founder-friendly valuations. Portage portfolio companies alone raised almost $1.2 billion of capital in the last 12 months from investors.

Along with the blockbuster funding, the total number of unicorns also surged in 2021. The total number hit 959 last year, a 69% increase from the year before.

The focus on vanity markers, such as unicorn status, was a sure sign that we were approaching a “top”. In the run-up to the dot-com bust, “number of eyeballs” (i.e., daily/monthly unique site visitors) was a much-touted metric. Similarly, this valuation status was an all-consuming pursuit, rather than one data point among several important others in the journey of building a great long-term business.

And now, sure enough, the end of the boom cycle has come. Expected interest rate spikes, high inflation, the ongoing pandemic, and geopolitical tensions are contributing to a tumultuous market. According to our calculations, public tech revenue multiples peaked in December 2021 at 7.85x P/S and, as of June 2022, they were at 5.15x, a reduction of 34% from peak levels thus far. We will likely not reach a bottom in the market until inflation peaks. A period of muddiness could then follow until the markets can see through to the next growth cycle.

How muddy might it get, and for how long? If the past is a prologue, we may be able to learn something from how tech stocks did during the dot-com bust and the global financial crisis (GFC). Public tech revenue multiples compressed by 75% in the dot-com bust and by 60% in the GFC. It wasn’t until November of 2014 that tech stocks recovered to their pre-GFC peaks. It wasn’t until August of 2021 that they recovered to the peaks they had hit before the dot-com bust.

While we can’t predict the future, as tech multiples head quickly toward their five-year median, it’s not unreasonable to believe that it will take years to reverse.

Being a wartime investor

You can’t be a wartime investor unless your entire team understands that they are on the battlefield. As a first step, ensure your team understands that the market environment has changed.

Turn the focus to your existing portfolio to understand who is most at risk and what actions need to be taken to mitigate failure. Align with other investors and management and get on with it—don’t wait for another quarter or two—regardless of your financial position. Wartime does not reward those pursuing a wait-and-see approach.

Realign internally where you invest future human and capital resources. Sadly, both are finite, and when sources of capital thin out, the power law of venture capital becomes a mission-critical consideration. Making the right big bets is doubly important in this environment because there is a higher likelihood that the companies already in your portfolio will be looking to you to lead or support their future rounds.

Shift your focus to targeted origination. Now is the time to refine and reprioritize your theses through deep research, market mapping, and customer due diligence. This is also the perfect time to build and rigorously test your investment theses.

Meet as many companies as possible. It boils down to understanding why you are a differentiated investor for a company and what actions you can take to drive its success.

Being a wartime CEO

If you lead a later-stage venture business, the first step is the same: ensure your team understands that the market environment has materially changed.

Hopefully, you took advantage of the previous robust market and have built a war chest that gives you runway for at least 24 months before requiring new funding. If you have the luxury to drive toward breakeven by sacrificing top-line growth—do it. If you do not, then get clarity on what the company needs to look like at the end of the runway to be attractive to future investors, who are likely to be more disciplined than those you saw in prior rounds.

This most likely means being able to demonstrate efficient growth, expanding gross and operating margins, and visibility into future profitability. In action, this translates to radical internal prioritization. You have to be resolute in cutting out activity that doesn’t immediately drive toward these three tenets.

If you are an early-stage business, it’s imperative that you align with your investors on what success looks like. This is especially important because, in many cases, your next investor will probably be your current investor. If you are able to raise externally, you will likely have demonstrated some form of product-market fit to a specific segment with a good understanding of your pricing power. And you probably have done so on a rather modest budget. You also probably started with an awesome, passionate, mission-driven team that is now starting to attract top talent. Finally, I bet you can articulate concisely how important and big your mission is and why you will be the winner.

A new world order

Some may find that making a quick buck from investing in the cutest CryptoKittie is more fun than pouring over spreadsheets or A/B testing, but that part of the cycle has passed.

But venture capital isn’t easy for investors or founders, nor is it supposed to be. We must understand and adapt to the shifts of a new cycle. When the next growth cycle comes, the commitment and support we show our highest-potential startups will pay off exponentially as multiples start to expand again.

Adam Felesky is the co-founder and CEO of Portage.

The opinions expressed in Fortune.com commentary pieces are solely the views of their authors and do not reflect the opinions and beliefs of Fortune.

請打開財富Plus APP